TaxCalc Blog

News and events from TaxCalc

New penalty regime: points mean prizes (for HMRC)

Updated 14/01/22 Following the latest ministerial statement regarding the new penalty regime we've updated the implementation date to 1 January 2023.

HM Revenue & Customs (HMRC) has confirmed that their new points-based penalty regime will come into effect from 1 January 2023 and will apply to both Making Tax Digital (MTD) for VAT as well as MTD for Income Tax Self Assessment (ITSA). Their stated aim is to make penalties simple, fair and effective but, as the arguably illustrious ageing rocker, Meat Loaf might say, "Two Out of Three Ain't Bad".

The new penalty regime covers late submission, late payment and interest harmonisation – and will usurp the existing rules in stages:

- For VAT taxpayers, from their first VAT return period starting on or after 1 January 2023.

- For ITSA taxpayers, from their first accounting period (or tax year) starting on or after 6 April 2023.

- For non-MTD Self Assessment taxpayers, from their accounting period (or tax year) starting on or after 6 April 2024.

Late submission

The new points-based system for late submissions is designed to be more lenient to those who make the occasional slip-up, whilst still penalising those who deliberately avoid their obligations.

When a taxpayer misses a submission deadline, they will incur a point. Once a penalty threshold has been reached, a fixed penalty amount of £200 will be issued for every missed submission until a period of compliance allows the points tally to be reset to nil.

All good so far, but this is where it starts to get complicated. Points accrue separately for VAT and ITSA so, although the regime is the same, points tallies and periods of compliance will need to be monitored independently. The points thresholds, and length of compliance periods, also vary depending on the frequency of submissions, as follows:

- Annual submissions (e.g. Self Assessment returns and VAT annual accounting): 2 points and 24 months compliance to reset

- Quarterly submissions (e.g. Quarterly ITSA updates and most VAT returns): 4 points and 12 months

- Monthly submissions (e.g. Monthly VAT returns): 5 points and 6 months

For the points to be reset to nil, as well as the necessary period of compliance that follows the last missed submission, all returns within the previous 24 months must be filed and up to date.

HMRC has confirmed that taxpayers can continue to appeal against penalties should they have a reasonable excuse.

Late payment

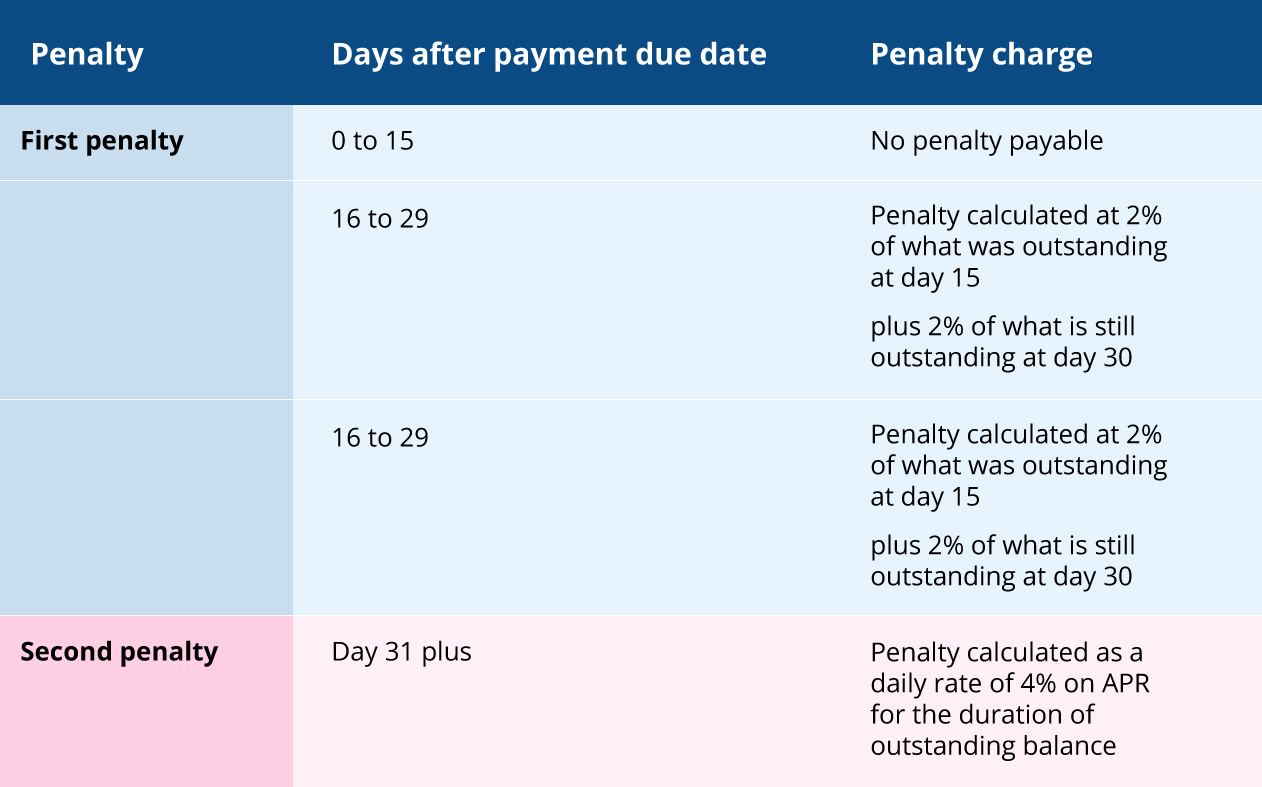

Late payment penalties will be more proportionate to the length of time payment is outstanding and can result in the defaulting taxpayer receiving two penalties depending on when payment is made.

The first penalty will be levied 31 days after the due date and the second penalty will be calculated on amounts outstanding from day 31 until the principal balance is paid in full. HMRC will notify the taxpayer of both penalties independently.

The first penalty is a fixed percentage calculated by reference to the amount outstanding on Day 15 and Day 30. The second penalty is calculated at a daily rate until the liability is settled, as illustrated below:

If taxpayers have agreed Time to Pay Arrangements with HMRC, then late payment penalties will not accrue.

For the first year of introduction only, no penalty will be levied if payment is made within 30 days of the due date, rather than 15.

Interest harmonisation

Independent of any penalties being levied, interest will accrue on any late payment from the tax due date until the date payment is received. VAT Repayment Supplement will be replaced with Repayment Interest. Repayment Interest will be paid from the later of:

- The due date of the return.

- The date the return is submitted.

And finally...

I shall leave it for you to decide whether HMRC will achieve its aims of simplicity, fairness and effectiveness in the tax system but, as Meat Loaf may also say "I would do anything for love, but I won't do VAT".

See how much you could save

Whether you're just getting started in practice, or an established firm see how much TaxCalc could save you.

Get a quoteRayburn 1957 (4 years ago)

Dean Shepherd (4 years ago)

How to subscribe

Get the TaxCalc news as soon as we publish it!

To sign up, please log in or create an account.

Log inHow to comment

If you already have a TaxCalc account, you can comment on any articles written here.

To avoid using your actual name, you can create a special ID. Just log in and visit your customer account to create it.

Create your IDAuthors

Article categories

(22)

(4)

(6)

(8)

(29)

(17)

(7)

(3)

(6)

(7)

(11)

(16)

(5)

(10)

(1)

(3)

(2)

(6)

(8)

(22)

(1)